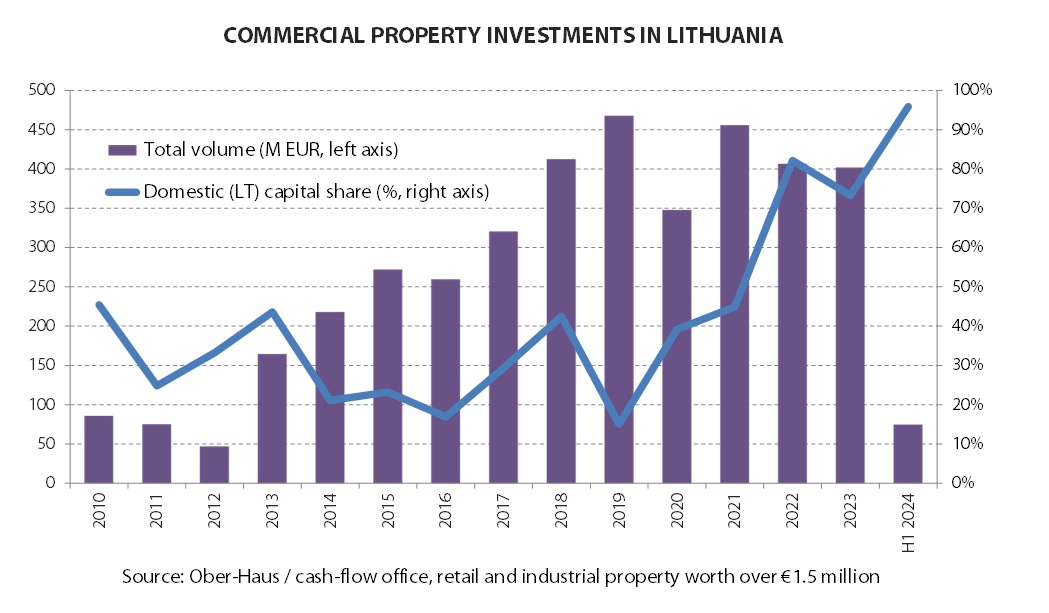

Optimism continues to be hard to find in the Lithuanian commercial real estate investment market, with overall performance falling to 10-year lows. “According to Ober-Haus, in the first half of 2024, EUR 75 million worth of modern flow commercial property (offices, retail, warehousing and industrial buildings and premises with a value of at least EUR 1.5 million) was acquired in Lithuania. The investment volumes for the first half of 2024 are 48% lower compared to the first half of 2023 and 71% lower compared to the second half of 2023. At the same time, the result for the first half of this year is the worst since the second half of 2013, according to the Ober-Haus review.

According to Raimonds Reginis, Research Manager for the Baltics at Ober-Haus, , the very significant percentage drop in investment volumes in 2024 was also due to the very high total result in 2023, which did not reflect the pessimistic mood prevailing in the property market in that year. And the higher than expected volume of investment transactions in 2023 is in fact due to one particularly large transaction.

At the end of 2023, it was announced that Baltic Opportunity, an investment company managed by Lords LB Asset Management, is acquiring six office buildings in Vilnius from Finnish company Technopolis (in 2018, London-based private equity real estate firm Kildare Partners agreed to acquire all of Technopolis shares). Technopolis entered the Lithuanian market in 2013 with the acquisition of 3 office buildings in the Ozo Park area and subsequently expanded its property portfolio in that area to 6 buildings with a total area of 106,000 sqm.

“The investment transaction was formally completed at the beginning of 2024, following the approval of the merger by the Competition Council of the Republic of Lithuania. However, given the factual circumstances, this transaction has been assigned to 2023 and can be said to have significantly changed the annual investment indicator in Lithuania”, says Reginis.

Although the details of the transaction were not disclosed, it is speculated that the value of this deal could have reached approximately EUR 200 million. In any case, this is the largest investment office transaction in Lithuania’s history, bringing the total volume of investment transactions in 2023 to EUR 402 million, only 1% less than in 2022 (EUR 406 million). Without this transaction, total commercial property investment in 2023 would have been twice as low, reflecting global trends that show commercial property investment in the main regions of the world contracting by around 50% in 2023.

In the first half of 2024, offices accounted for the largest share of investments

Meanwhile, the result for the first half of this year is modest and fairly accurately reflects the generally pessimistic mood in the real estate market. The investment transaction market has been dominated this year by small transactions, mostly in the EUR 3-6 million range. According to Ober-Haus estimates, the office segment accounted for the largest share of investments in the first half of the year with EUR 34 million, or 46% of total investments for the first half. The largest investment transactions of the half year were in this segment.

At the beginning of the year, real estate development company Eriadas, together with DIFF Develop, a closed-end investment company for informed investors, acquired the buildings of the headquarters of insurance company Ergo in Vilnius, Geležinio Vilko Street. Ergo plans to continue renting the premises from the new owners while looking for new premises for its employees. Meanwhile, the new owners of the buildings and land have plans for a new commercial and residential development on the site.

The largest transaction was completed in mid-2024, when the fund of the investment management company ZeroSum Asset Management acquired a complex of three office buildings in Vilnius, Švitrigailos street from the Norwegian company AMG Property. As the Norwegian company sold its previous properties in 2022, this was the last property in Lithuania it managed.

Investors focused on small format shops

In the first half of this year, the volume of investment in retail property acquisitions accounted for 34% of all commercial property investment in Lithuania. Although there were no major acquisitions in this segment, buyers were quite active in acquiring modern small format stores (1,500-2,500 sq m) located in large food chains.

There have been five such acquisitions in Lithuania in the last six months, with the largest deal initiated by supermarket chain Lidl, which agreed to sell four of its newly built stores to a fund managed by investment management company DIFF Assets. The acquisition of three stores was actually completed in the first half of this year and the acquisition of the fourth is expected to be completed in the second half of this year.

“Despite the noticeable stagnation in the investment property market, such properties remain popular among buyers. Strategically located supermarkets, which are operated by major retail chains, virtually guarantee a stable rental income stream for new owners and a tenant with an interest in continuity. For example, in just the past two and a half years, nearly 30 supermarkets of this format have changed owners in Lithuania”, says Reginis.

The remaining 20% of investment in the first half of this year was in the acquisition of warehousing and industrial properties. The largest transaction took place in Kaunas, where the fund of investment company Eika Asset Management sold a 5,600 sqm logistics building to pharmacy chain Camelia, which is leasing it.

Foreign investor activity shrinks to a minimum

The current mood in the country’s commercial property investment market is reflected not only in the amount invested or the number of properties acquired, but also in the origin of the investment capital.

In 2022-2023, a record increase in the share of local investors in the Lithuanian investment market was observed, indicating that foreign investors significantly reduced their investments in real estate in our country. In 2022, the share of capital owned by Lithuanians have increased to 82%, while in 2023, it accounted for 73%. In the first half of 2024, the share of local capital increased to 96%, showing that the market is essentially left to local investors. For example, from 2012 to 2021, the share of local investors in total investments was only 37%.

The range of profitability indicators is significantly wider

In an environment of extremely low volumes and low diversity of investment transactions, it is difficult to objectively assess changes in investment property yield in the first half of this year.

“Some of the transactions indicate that investors are still willing to pay record prices for their currently most attractive assets (e.g. supermarkets), but less attractive assets (older properties or properties with other uses) are being acquired at yields that are more attractive to buyers (at a lower price than before). It can be said that the yield spread has now widened significantly, meaning that overall commercial property yields have tended to rise slightly this year”, says Reginis.

Outlook for the second half of the year: passive investors and uncertain return of foreign capital

Looking at the results of the first half of this year and the general investment climate (especially investors’ expectations), it is unlikely that we can expect a surge in the number of investment transactions in the second half of the year.

According to Reginis, it is unlikely that there will be a return of foreign investors to our market this year, or any bolder decisions on the part of local investors. “However, technically at least, total volumes will not necessarily remain at the lows of the first half of this year. For example, one or more large investment deals can significantly raise the overall investment volume indicator (as we saw in 2023),” says an Ober-Haus analyst.

It should also remembered that in recent decades a number of property funds with a foreseeable life have been invested in commercial property. When the fund’s specified operating period ends (e.g., 5 years), the fund manager sells the real estate on the market and settles with the investors, or, if an agreement with the investors is reached, extends the fund’s operations for a certain period (e.g., 2 years). The commercial assets sold by the funds to be closed in the near future would provide a clearer picture of the overall liquidity of the property market and the value of these assets in the current environment.

Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.4% in June 2024. The overall level of apartment prices in Lithuania’s major cities has grown by 3.3% over the last 12 months (annual growth of 2.7% in May 2024).

In June 2024, the sales prices of apartments in Vilnius, Kaunas, Šiauliai and Panevėžys grew by 0.5%, 0.7%, 0.9% and 0.3%, respectively, and the average price per square metre amounted to EUR 2,615 (+12 Eur/m²), EUR 1,778 (+12 Eur/m²), EUR 1,131 (+11 Eur/m²) and EUR 1,103 (+3 Eur/m²). Meanwhile, Klaipėda recorded a 0.1% decrease in apartment prices in June, with the average price per square metre amounting to EUR 1,687 (-2 Eur/m²).

Over the year (June 2024 compared to June 2023) apartment prices increased in all major cities of the country: in Vilnius – 2.5%, in Kaunas – 3.2%, in Klaipėda – 5.3%, in Šiauliai – 4.9%, and in Panevėžys – 4.2%.

“Looking at the sales price curve for housing in major cities in recent years, it can be seen that it is broadly in line with the price dynamics of consumer goods and services in the country. According to the State Data Agency, the annual inflation rate calculated on the basis of the Harmonised Index of Consumer Prices in June 2024 was 1.0%, while the selling prices of apartments grew by 3.3% over the same period. This means that real selling prices of apartments in the country’s major cities rose by 2.2% over the year, net of inflation.

And despite the significant rise in nominal terms in apartment prices over the last three years (36.5%), this increase did not stand out in the context of the country’s overall inflation (31.8%). That is to say, over the three years, real selling prices of apartments in the country’s major cities increased by only 3.4%. This has been the longest period with the smallest gap between the change in house prices and inflation and, historically speaking, we have only seen a very similar situation in the 2013-2015 period. This is good news for potential homebuyers, as real wage growth has accelerated and housing affordability indicators are slowly improving as inflation has receded,” says Raimondas Reginis, Research for the Baltics at Ober-Haus.

The year 2023 was full of challenges for the real estate markets of the Baltic countries showing some early signs of this back in 2022. Last year, Baltic countries saw an economic slowdown, declining activity in the residential and commercial real estate market, rising number of unsold apartments, higher office vacancy rates and slowing construction volumes. According to the Ober-Haus annual Real Estate Market Report on the capital cities of the Baltic countries, it is clear that the sentiment of homebuyers, businesses and investors alike has slumped and confidence in the Baltic real estate market as a whole has further eroded.

While the general sentiment of the real estate market participants is similar across the Baltic countries, the overall impact of global factors (Russia-Ukraine war, high inflation, interest rate hikes) differs to a varying degree.

“Since the real estate market in Latvia and its capital city has lacked fast growth in the last five years, the impact of the current challenges is not as tangible as in other countries,” Raimondas Reginis, Head of Market Research for the Baltics at Ober-Haus, said. Meanwhile, real estate markets in Estonia and Lithuania experienced an investment boom in the aftermath of Covid-19, resulting in a very rapid growth in the housing market activity and a surge in prices. Therefore, the slowdown of the last few years has been most felt in the markets of Lithuania and Estonia, which have moved into a much slower phase of development, particularly noticeable among market participants who got accustomed to a period of record activity. According to Reginis, the market slowdown is particularly steep in Estonia, where after a slight recession in 2022, the economy contracted by as many as 3% in 2023. Unlike in Latvia and Lithuania, recovery is not expected in Estonia this year. This does not only mean a weaker sentiment in the property market in this country, but also affects the general expectations of the population, which remain among the lowest in Europe.

Despite the more challenging period, real estate markets in the Baltic countries have managed to avoid the worst-case scenario, which is usually characterised by a substantial decline in rents or sales prices.

“A fairly stable situation in the labour market, real wage growth, solid savings of the population and the low overall level of indebtedness have protected real estate market participants from hasty decisions or emergency choices and, at the same time, from negative price changes. It is clear, however, that over the last few years, buyers have significantly strengthened their positions in the market and are often the ones who dictate the terms rather than sellers. Therefore, sellers who need to dispose of their property more quickly remain in a more difficult situation,” Reginis noted.

The analysis of the completed housing transactions shows that a small number of potential buyers are able to take advantage of this situation and purchase homes at prices slightly lower than those normally seen in the market. A similar situation can be observed in the commercial real estate market, where the number of investors (particularly foreign investors) has dropped and the yield on commercial real estate has increased by around 50-100 basis points in 2023 alone.

The first half of 2024 has not made real estate market participants more optimistic, because the key market indicators of the last few years remain low and it may take a little longer than previously expected for the real estate market to regain the confidence of market participants. “It is therefore clear that in 2024 both first-time home buyers and larger investors will still be able to find attractive offers on the real estate market of the Baltic countries. It is important not to miss this opportunity, because the real estate market is not stagnant and there are plenty of buyers looking for the best option on the market,” Reginis added.

Read more in the 2024 Ober-Haus annual Real Estate Market Report on the capital cities of the Baltic countries. The report covers the office, retail, warehousing, residential and land markets in each of the capital cities – Riga, Tallinn and Vilnius. The report also includes a section on taxes prepared by the audit, accounting and consultancy company PricewaterhouseCoopers and a section that contains legal information prepared by Sorainen Law Firm.

Full review (PDF): Baltics Real Estate Market Report 2024

Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.1% in May 2024. The overall level of apartment prices in Lithuania’s major cities has grown by 2.7% over the last 12 months (annual growth of 2.8% in April 2024).

Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.1% in May 2024. The overall level of apartment prices in Lithuania’s major cities has grown by 2.7% over the last 12 months (annual growth of 2.8% in April 2024).

In May 2024, the sales prices of apartments in Klaipėda, Šiauliai and Panevėžys grew by 0.5%, 1.0% and 1.2%, respectively, and the average price per square metre amounted to EUR 1,689 (+8 Eur/m²), EUR 1,120 (+11 Eur/m²) and EUR 1,100 (+13 Eur/m²). Meanwhile, Vilnius recorded a 0.1% decrease in apartment prices in May, with the average price per square metre amounting to EUR 2,603 (-2 Eur/m²). In Kaunas, the average price per square metre remained unchanged at EUR 1,766 per square metre.

Over the year (May 2024 compared to May 2023), apartment prices grew in all major cities of the country: in Vilnius – by 1.8%, in Kaunas – by 2.7%, in Klaipėda – by 5.2%, in Šiauliai – by 4.0%, and in Panevėžys – by 4.1%.

“It can be said that the Lithuanian housing market has already reached its lowest point of activity in the last few years. In May this year, even after a 26-month break, a positive annual change in activity was recorded, when more apartments were purchased in Lithuania than a year ago. Of course, the annual increase in activity is not significant (1.2%), but it is already the first sign of a stabilised housing market. But the number of transactions is still at its lowest point since 2015 and at the moment both sellers and buyers are not showing much optimism.

Despite the continued sluggishness in the housing market, sellers are still managing to sell their homes at slightly higher prices than before. They just have to accept a noticeably longer selling period as the market continues to suffer from a lack of firmly committed buyers. And looking at the situation in the country’s housing market over the last two years, the patience of home sellers has paid off and the majority of buyers have not been able to get lower prices.

As expected, in June this year the European Central Bank (ECB) cut its key interest rates for the first time after a long pause. This is one of the most anticipated decisions for real estate market participants, who have been living in a shrinking market environment for the last two years and have been waiting for something that could change this situation. The ECB’s decision to cut interest rates is in itself a positive signal for housing market participants (both sellers and buyers), but the level of the interest rate change does not mean that from now on we will see a rapid return of buyers to the market or rising investment in new housing development. The burden of servicing loans for borrowers or those planning to borrow has already started to ease since the end of 2023, when we saw a gradual decline in the EURIBOR rate. Obviously, that first drop in interest rates has not yet had a major impact on homebuyers’ decisions and they are waiting for a bigger incentive, either more attractive house prices or a more tangible drop in interest rates.

Market participants do not hold out much hope that the ECB will cut interest rates again in July this year and are hinting at a less frequent pace of rate cuts. Therefore, it can be predicted that the recovery of the housing market will also be delayed and that at least the summer period of this year will not be characterised by any major changes in house prices or market activity”, says Raimondas Reginis, Research for the Baltics at Ober-Haus.

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.2% in March 2024. The annual apartment price growth in the biggest cities of Lithuania was 2.4% (a 2.2% increase was recorded in February 2024).

In March 2024 apartment prices in Vilnius, Klaipėda, Šiauliai and Panevėžys increased by 0.2%, 0.7%, 0.4% and 0.5% respectively, with the average price per square reaching EUR 2,593 (+4 EUR/sqm), EUR 1,662 (+11 EUR/sqm), EUR 1,100 (+5 EUR/sqm) and EUR 1,081 (+6 EUR/sqm). In the same month, apartment prices in Kaunas decreased by 0.1%, and the average price per square meter dropped to EUR 1,749 (-2 EUR/sqm).

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 1.9% in Vilnius, 2.7% in Kaunas, 3.8% in Klaipėda, 1.9% in Šiauliai and 2.3% in Panevėžys.

“Despite the continued decline in overall activity in the country’s housing market, house sales prices in the country’s major cities are showing resilience and are even managing to continue to climb upwards slowly. According to the data of the State Enterprise Centre of Registers, in the first quarter of 2024, compared to the first quarter of 2023, there will be 13% fewer purchases of both flats and houses in Lithuania. In the same period, almost 5% fewer older apartments were purchased, while 40% fewer acquisitions of newer apartments were registered in the country. The decline in new housing construction, which started in 2023, means that this year there are significantly fewer apartment transactions in new construction projects. This also leads to a greater overall decline in housing market activity.

The fact that sales prices of apartments have recently remained broadly stable or even managed to increase is well illustrated by the price dynamics of the largest and most popular housing segment in the country’s major cities. “According to Ober-Haus estimates (based on registered sale-purchase transactions), in the first quarter of 2024, the median selling price per square metre of 2-room apartments in old-built apartment blocks in typical residential districts of Vilnius was EUR 1,939/sqm, or 1.9% more than in the same period in 2023. In the same period in Kaunas, the median selling price per square metre of such apartments was EUR 1,416 per square metre (1.7% more than in the first quarter of 2023), and in Klaipėda – EUR 1,316 per square metre (7.4% more than in the first quarter of 2023).

This shows that, despite the generally negative sentiment still prevailing in the property market, home sellers are able to withstand the pressure from potential buyers and are not making any major adjustments in the selling price. So far, we observe that some home sellers are trying to adapt to the slower market pace and are adjusting their over-optimistic expectations. However, those sellers whose properties are sold at market price sooner or later find their buyers. It is the sellers’ calmness and their ability to wait longer for buyers that is responsible for the fact that the overall change in house prices in the country’s major cities continues to be positive, albeit with a slight upward bias,” says Raimondas Reginis, Research Manager for the Baltics at Ober-Haus.

Full review (PDF): Lithuanian Apartment Price Index, March 2024

Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.2% in February 2024. The overall level of apartment prices in Lithuania’s major cities has grown by 2.2% over the last 12 months (annual growth of 2.1% in January 2024).

Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.2% in February 2024. The overall level of apartment prices in Lithuania’s major cities has grown by 2.2% over the last 12 months (annual growth of 2.1% in January 2024).

In February 2024, the sales prices of apartments in Vilnius, Kaunas and Klaipėda grew by 0.3%, 0.3% and 0.1%, respectively, and the average price per square metre amounted to EUR 2,589 (+8 Eur/m²), EUR 1,751 (+6 Eur/m²) and EUR 1,651 (+1 Eur/m²). Meanwhile, Šiauliai recorded a 0.2% decrease in apartment prices in February, with the average price per square metre amounting to EUR 1,095 (-3 Eur/m²). In Panevėžys, the average price per square metre remained unchanged at EUR 1,075 per square metre.

Over the year (February 2024 compared to February 2023), apartment prices grew in all major cities of the country: in Vilnius – by 1.8%, in Kaunas – by 3.2%, in Klaipėda – by 3.0%, in Šiauliai – by 1.7%, and in Panevėžys – by 1.8%.

“Although the cold snap that has gripped the country’s housing market is not going away yet, one indicator that is important for homebuyers is already showing positive changes. In 2023, the housing market was largely chilled by extremely high interest rates on loans, which reduced the ability of homebuyers to afford to buy with borrowed money. However, looking at the house price-to-wage ratio, in 2023 this indicator started to improve for homebuyers after a two-year hiatus. According to the State Data Agency, in 2023, the average monthly net wage in the five largest cities of the country will grow by 10.5-11.6%, while the average annual growth in the selling prices of apartments in these cities, according to the Ober-Haus data, will reach 6.2-9.1%. Faster wage growth has finally led to a slight improvement in the affordability index in all the country’s major cities.

In 2023, a statistical resident of Vilnius could buy a middle-class apartment in Vilnius of 6.7 sqm (6.6 sqm in 2022) for average net annual salary. In Kaunas, the figure was 9.0 sqm (8.8 sqm in 2022), in Klaipėda – 9.3 sqm (8.9 sqm in 2022), in Šiauliai – 12.3 sqm (11.8 sqm in 2022) and in Panevėžys – 12.9 sqm (12.3 sqm in 2022). Thus, in 2023, a metropolitan resident could already buy 0.1-0.6 sqm more than in 2022.

Looking at the dynamics of house sales prices in 2023 and at the beginning of 2024, we can see that the monthly price increase remains very small, so that the annual price change has fallen to the 2% level. Unless we see a faster recovery of the housing market in 2024, it is realistic to expect an average annual growth of around 2-3% in apartment sales prices this year.

Meanwhile, economists predict that by 2024, the country should see rapid wage growth, which could reach 8-10%. This means that if in 2024 wages were to grow several times faster than house prices, we would see a noticeably faster improvement in the affordability index than last year. Then, in Kaunas, Klaipėda, Šiauliai and Panevėžys, people would be able to buy the same amount of housing for their salaries as in 2020, when the ratio of apartment prices to salaries was the most favourable. Meanwhile, in Vilnius, the affordability ratio is likely to recover more slowly, as apartment prices in the capital city grew faster than in other major cities in the country in 2021-2023. The increase in housing prices in Vilnius is not only driven by the long-standing internal migration factor, but also by the very large number of newcomers from other countries from 2022 onwards. Therefore, the increase in population in the capital in recent years means that there is still a strong demand for housing, which may not allow the housing affordability index to improve as fast as in other major cities in the country,” says Raimondas Reginis, Research for the Baltics at Ober-Haus.

Over the past few years in Lithuania, we have seen a rapid decline in housing market activity, which has impacted the volume of new housing developments. However, apartment building developers in the country’s major cities have been facing the toughest challenges lately, with very modest apartment sales figures in the period 2022–2023. According to Ober-Haus, compared to the record activity of 2021, in 2023, the sales of apartments in the primary market were down by 68% in Vilnius, 55% in Kaunas, and 57% in Klaipėda.

“Despite the two- to three-fold decrease in the sales of newly-built apartments, a very high number of apartments were nevertheless completed in the country’s major cities in 2023, because the development of these projects had begun during 2021 and 2022,” said Raimondas Reginis, Head of Market Research for the Baltics at Ober-Haus.

According to Ober-Haus, in 2023, developers in Vilnius built 4,915 apartments for sale – 18% more than in 2022. When considering the last two decades, this is one of the highest figures, second only to those in 2007, 2008 and 2020, when more than 5,000 apartments were built for sale. In 2023, 52 different apartment projects (including ongoing project phases) were available for buyers in Vilnius.

The largest construction volumes of apartments for sale and for rent are concentrated in the capital city Vilnius. Following high development activity in 2022, the property rental segment saw a surge in 2023. Two new rental projects (Solo Society City House Vilnius and Atlas Co-living) were completed there. They offered almost 800 units to the market bringing the total number of professionally managed units for rent to 2,100. Ober-Haus estimates that two more projects will be completed in Vilnius (Vytenio Street and Talino Street) in 2024, offering almost 300 units for rent.

“Since many people in recent years have postponed buying a home, renting remains a relevant and affordable option for many looking for a home. Therefore, the rapidly expanding professionally managed rental segment allows the balance between supply and demand in the real estate market to be maintained,” Reginis explained.

In 2023, construction projects were predominantly developed in the residential districts of Vilnius, while the volume of construction projects in the Old Town of Vilnius was the most modest of the last decade

Developers completed new apartments in 18 out of 21 neighbourhoods within the City of Vilnius in 2023. Slightly more than half of the total number of apartments were built in five neighbourhoods: Verkiai (14.6%), Rasos (10.1%), Pašilaičiai (9.5%), Viršuliškės (8.4%) and Lazdynai (8.7%).

In 2023, very low construction volumes were recorded in the Old Town of Vilnius (0.8%), one of the most modest indicators over the last decade for this area. Reginis notes that in previous years many more apartments were built for sale in the Old Town, due largely to the conversion project in the Paupys district. The real estate development company, Darnu Group, built more than 800 apartments for sale on the former Skaiteks factory site in the period 2020–2022. Other companies also actively developed apartment building projects in Paupys and the adjacent Užupis area during this period. In 2023, however, only a few projects were instigated in the Old Town, some of which took longer than planned or were even suspended. According to the Ober-Haus expert, an increase in supply can be expected in 2024–2026, when the projects currently in progress or planned for the near future will be completed.

For the first time in history, the average size of apartments in Vilnius is below 50 sqm

For the first time during the entire period of reporting on property by Ober-Haus (over 20 years), the average size of apartments built for sale did not exceed 50 sqm. According to Ober-Haus, in 2023, the average floor area of individual apartments in apartment buildings built in Vilnius was 49.9 sqm. For example, during 2020–2022, the average floor area of apartments in newly developed apartment buildings was 52-53 sqm.

“The very small average size of apartments built in 2023 could be attributed to the structure of housing under construction. Often, higher-end projects and projects in prestigious areas of the city offer more spacious apartments, but there were very few such projects in 2023,” Reginis noted.

Looking at other major cities in the country, we can see similar long-term trends to those in Vilnius, i.e. smaller apartments with fewer rooms are built for sale. However, the average floor area is still higher than in Vilnius. “According to Ober-Haus, in 2023, the average floor area of an apartment in residential buildings built in Kaunas was 54.7 sqm and in Klaipėda, it was 54.6 sqm.

A++ energy performance class apartment buildings will dominate in 2025

Although the requirement to comply with A++ energy performance class for new buildings came into force 1 January 2021 (for obtaining a building permit), there were still relatively few such apartment buildings built in Vilnius in 2023. Data collected by Ober-Haus, show that apartments in A++ energy performance class buildings accounted for only 22.4% of the total number of apartments built for sale in Vilnius in 2023 (5.3% in 2022). Apartments in A+ energy performance class buildings accounted for 56.9% of the total number of apartments built for sale in Vilnius in 2023 (70.4% in 2022). Apartments in A energy performance class buildings accounted for 12.3% of the total number of apartments built for sale in Vilnius in 2023 (17.4% in 2022). The remaining apartments (8.4%) were built in B energy performance class apartment buildings or lower (6.9% in 2022).

“Under half of total number apartments will be built in A++ energy class apartment buildings in 2024. This means that the highest energy class apartments will only start to dominate the primary market in Vilnius from 2025,” Reginis commented.

Forecast confirmed, with a record number of apartments built in Kaunas

The forecasts made a year ago concerning record volumes of newly built apartments in Kaunas were fully realised in 2023. According to Ober-Haus, developers in Kaunas built 1,479 apartments for sale in 2023, or a significant 45% more than in 2022. Historically, this is the highest number of apartments built for sale per year in this city. The threshold of 1,000 newly built apartments was only exceeded in 2008 (1,070 apartments) and in 2022 (1,020 apartments). In total, 31 different projects (including ongoing project phases) were offered to buyers in Kaunas in 2023.

In 2023, developers built apartment blocks in various locations in and around Kaunas, but a total of 23% of all apartments were built in the Aleksotas neighbourhood. This was due to the completion of several large-scale projects in this area: the first phase of the Nemunaičiai project in H. and O. Minkovskių Street (around 160 apartments) and the Europos Sodas project (around 130 apartments). Construction was in progress in other districts of the city too: a total of 70% of the apartments were built in the districts of Šančiai, Dainava, Vilijampolė, Žaliakalnis, Eiguliai and the city centre.

Analysis of developers of apartment buildings shows that local companies investing exclusively in Kaunas dominated, while small and usually little-known companies developed smaller scale apartment building projects. “As a result, to continue to improve the transparency of the city’s housing market and to increase the quality or scale of the projects, it is important to attract financially stronger and nationally known developers who are capable of implementing truly ambitious projects,” Reginis explained. YIT Lietuva, Citus, SBA Urban, and others, are some of the companies that continue to actively invest or are taking their first steps in the Kaunas housing market.

The development of various apartment projects exclusively for rent, in addition to projects developed for sale, is one of the qualitative evolutionary steps for the housing market in Kaunas. In mid-2023, the real estate development company, the Etapas Group, completed the construction of five apartment buildings on Žeimenos Street in the Eiguliai district. Three of the apartment buildings were offered for sale. The Estonian capital investment company, Eften Capital, invested in the construction of the other two buildings offering 96 apartments for long-term rent. Ober-Haus estimates that currently there are around 550 professionally managed apartments for rent in Kaunas.

Development rates in Klaipėda remain stable – over 400 apartments per year

According to Ober-Haus, developers in Klaipėda built 402 apartments for sale in 2023 or 14% less than in 2022. There has not been any significant breakthrough in apartment development in Klaipėda for more than a decade. Since 2009, the number of apartments built for sale in Klaipėda has not exceeded 500 apartments per year (the highest number built during this period was in 2022 – a total of 466 apartments). In total, 10 different projects (including ongoing project phases), were offered to buyers in Klaipėda in 2023.

Reginis points out that despite the small volume of developments for apartment buildings, particularly compared to Vilnius or Kaunas, there finally are tangible results in terms of investment in the central part of the city of Klaipėda.

Eriadas, a construction management and real estate development company, is finishing the Parko Pakrantės project near Malūnas Park (4 out of 5 apartment buildings were completed in 2023). In 2023, the company began the construction of the Bastionų Namai project with over 700 apartments near the River Danė (the first two apartment buildings are scheduled for completion in 2024). In the second half of 2023, Stemma Management started the construction of the ambitious Memel City project at the junction of the River Danė with the Curonian Lagoon. The first phase consists of the construction of just over 100 apartments and a business centre. The completion of the first apartment buildings is scheduled for 2025.

“This investment is particularly important for Klaipėda, because the construction of higher-class residential property in the central part of the city can revitalise both Klaipėda’s Old Town and the adjacent areas, where smaller businesses such as restaurants, cafes, services companies, etc. usually operate, and where higher-income residents are their main clients,” Reginis explained.

In general, Klaipėda has not been able to boast any significant positive demographic trends over the last decade. According to the latest data from the State Data Agency, Statistics Lithuania, the number of permanent residents in the municipal area of the city of Klaipėda has increased by only 0.8% over the last decade, or just over 1,300 inhabitants. Meanwhile, the population of Klaipėda District grew by 33.2% or almost 16,800 inhabitants over the same period. This highlights that the development of the Klaipėda region can be attributed to the population growth in the districts surrounding the city rather than the population growth in the city. The actual figures for construction volumes also confirm that over the last decade, 2.6 times more residential real estate (houses and apartments) was built in the Klaipėda region than in the city itself.

2024 can be characterised by much more modest construction volumes

When considering the volume of apartment construction in 2024 in the two largest cities in the country (Vilnius and Kaunas), the observable trend is opposite to that of 2023. Given the number of apartments currently under construction, Ober-Haus estimates that in 2024, a total of around 2,900 apartments will be built for sale in Vilnius, or 41% less than in 2023. A similar slowdown in construction volumes is expected in Kaunas, where around 850 apartments are expected to be built in 2024 (43% less than in 2023).

Reginis observes that the last time such low construction volumes were recorded in Vilnius was in 2014, while in Kaunas, it was during 2019–2020. “It is obvious that the low apartment sales volumes in the primary market in the last two years, and the very rapid increase in interest rates, have forced a number of developers to abandon their development plans or reduce the pace of their developments,” the expert said.

At the same time, in Klaipėda, the volume of apartment construction in 2024 will remain at a similar level to that during 2022–2023. According to Ober-Haus, about 420 apartments will be built in Klaipėda – slightly more than in 2023. Unlike Vilnius or Kaunas, Klaipėda has not seen a significant breakthrough in apartment construction since 2009, and there is no slowdown as such, since construction volumes remain at a relatively low level.

Overall, looking countrywide, there is a clear trend towards significantly decreased volumes of residential property construction. According to the State Data Agency, the number of apartments where construction was started in 2023 was 42% less and the number of houses reduced by 26% in comparison to 2022.

Inevitably, such a significant slowdown in housing development will have negative consequences for the overall market. For example, the construction segment in this sector of real estate will have significantly fewer orders than in previous years, and potential homebuyers will have fewer choices.

“If we see a stronger recovery of the housing market in 2024, but developers fail to respond by offering more housing, then the market could experience a greater shortage at some point. This would cause housing prices to increase again more rapidly. In addition, there is the recently widely discussed potential demand for accommodation in Vilnius and Kaunas to house the German brigade and their families due to arrive in Lithuania. Therefore, it is now crucial that businesses prepare for a faster market recovery scenario to prevent the market from becoming out of balance once again,” Reginis concluded.

Unique Properties, a real estate development company, has received a permit and started the construction of the Vilniaus Džiazas project in K. Vanagėlio Street in Vilnius Old Town.

K. Vanagėlio str. 11 and 18, which consists of a two-storey apartment building with 62 apartments and 11 commercial premises, a 1200 sqm administrative cultural heritage object of interwar construction and public spaces. The project will feature apartments with 4,5 m high ceilings and 4 m high stained-glass windows, the ground floor will have private patios and access to a garden, while the second and third floors will have balconies and the last floor will have private terraces.

According to Gediminas Tursa, CEO of Unique Properties, Vilniaus Džiazas aims to revitalise a part of the Old Town that was undeservedly forgotten during the Soviet era, and to reconnect it with the Rasa. The complex not only includes an open and lively commercial street along the north-south axis, but also new pedestrian and cycling connections to the railway station.

“After obtaining the building permit, the company received a lot of interest from interested parties and within a couple of weeks it sold several more apartments – currently Vilniaus Džiazas has signed about 20 preliminary contracts for apartments and sold several commercial premises. The price per square metre of apartments in the project varies between EUR 5,000 and EUR 12,000,” says Sandra Grinkienė, Real Estate Project Manager at Ober-Haus.

Financial partners are also showing their confidence in the Vilniaus Džiazas project. “Construction work is being started with our own and interim financing, and agreements are being finalised for further financing, including bank financing. Even against the backdrop of a more moderate housing market, we can feel the strong confidence of buyers and lenders in the exceptional architecture,” says Mr Tursa.

Construction of the entire complex is expected to be completed in the third quarter of 2025. Unique Properties is investing a total of approximately EUR 23 million in the complex.

Vilniaus Džiazas was designed by Do Architects, construction management is being handled by Incorpus, and Sorainen is advising on legal matters. Ober-Haus is taking care of the commercial and marketing aspects.

More about the project www.vilniausdziazas.lt

Ober-Haus Lithuanian Apartment Price Index (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.3% in January 2024. The overall level of apartment prices in Lithuania’s major cities grew by 2.1% over the last 12 months (annual growth of 1.7% in December 2023).

In January 2024, in Vilnius, Kaunas and Klaipėda, the sales prices of apartments grew by 0.2%, 0.5% and 0.6%, respectively, and the average price per square metre amounted to EUR 2,581 (+6 Eur/m²), EUR 1,745 (+9 Eur/m²), and EUR 1,650 (+10 Eur/m²). Meanwhile, Šiauliai and Panevėžys recorded a decrease of 0.1% and 0.6% respectively in January and the average price per square metre was EUR 1,098 and EUR 1,075 (-6 Eur/m²).

Over the year (January 2024 compared to January 2023) apartment prices increased in all major cities of the country: in Vilnius – 1.6%, in Kaunas – 3.0%, in Klaipėda – 2.8%, in Šiauliai – 2.3%, and in Panevėžys – 1.7%.

The Ober-Haus Apartment Price Index (OHBI) in Lithuania, which records changes in apartment prices in five major Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), increased by 0.5% in December 2023. Overall, the apartment prices in the major cities of Lithuania have increased by 1.7% over the last 12 months. The average annual apartment price increase in 2023 (January-December year-on-year) stood at 8.2%.

In December 2023, apartment sales prices in Vilnius, Kaunas, Klaipėda and Panevėžys increased by 0.4%, 0.6%, 0.8% and 0.8% respectively and the average price per square meter in these cities was EUR 2,575 (+11 EUR/sqm), EUR 1,736 (+10 EUR/sqm), EUR 1,640 (+13 EUR/sqm), and EUR 1,081 (+8 EUR/sqm). In Šiauliai, apartment sales prices decreased by 0.7% and the average price per square meter was EUR 1,098 Eur (-8 EUR/sqm).

Apartment prices rose year-on-year in December 2023 in all major cities of the country: 1.1% – in Vilnius, 2.7% – in Kaunas, 2.4% – in Klaipėda, 2.4% – in Šiauliai and 2.0% – in Panevėžys

“Despite the decrease in the number of sales transactions in the Lithuanian housing market by 14% for two consecutive years, the country avoided a decline in the sale prices in 2023. In the course of the year, only minor positive or negative monthly changes in the sales prices of apartments were recorded, resulting in a symbolic overall annual price increase of 1.7%. The last time even lower annual price increase was recorded in the country’s major cities was ten years ago, in December 2013, and stood at 1.1%. Since apartment sales prices remained record high throughout the year, the average annual change in 2023 remained quite solid – at 8.2%. Looking at the results of the last decade, a faster average annual growth of apartment prices in the country’s major cities was recorded only in 2021 (14.2%) and 2022 (21.5%). Overall, the sales price curve for apartments in 2023 coincided with the national inflation rates and almost replicated the changes in prices of other consumer goods and services.

Looking at individual cities or housing segments in the country, the overall trends in price changes during the year were almost identical. A rapid slowdown in price growth was recorded across all major cities and housing segments. Despite the low activity of the primary apartment market and the discounts and various gifts offered by developers, the prices for newly build apartments in 2023 increased slightly more than the prices of older apartments, an increase of 3.2% and 0.7% respectively.

Even the subdued mood and the noticeable drop in activity on the property market did not force the majority of the sellers to actually reduce their prices and as the year progressed housing market participants essentially moved into the waiting mode. Potential buyers were waiting for a clearer geopolitical situation, lower mortgage rates or lower house prices, while sellers expected buyers to return to the market in the future and waited patiently for them. Meanwhile, housing developers were as active as ever in promoting their properties and offering various benefits to buyers, and reduced the volume of new developments. If there is a turnaround in the market expected by sellers and buyers in 2024 and buyers return to the market, a negative annual change in house prices is likely to be avoided. However, taking into account all the existing global or local challenges, it is possible that the recovery of the housing market will not necessarily be sudden and it will take longer than expected for the buyers’ willingness and capacity to buy homes to recover,” says Raimondas Reginis, Head of Market Research for the Baltics, Ober-Haus.