The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.5% in March 2025. The annual apartment price growth in the biggest cities of Lithuania was 4.3% (a 4.1% increase was recorded in February 2025).

In March 2025 apartment prices in Vilnius, Kaunas, Šiauliai and Panevėžys increased by 0.4%, 1.3%, 0.4% and 0.2%, respectively, with the average price per square meter reaching EUR 2,680 (+10 EUR/sqm), EUR 1,846 (+24 EUR/sqm), EUR 1,172 (+4 EUR/sqm) and EUR 1,149 (+2 EUR/sqm). In the same month, apartment prices in Klaipėda decreased by 0.1% and the average price per square meter dropped to EUR 1,752 (-2 Eur/sqm).

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 3.3% in Vilnius, 5.6% in Kaunas, 5.4% in Klaipėda, 6.5% in Šiauliai and 6.4% in Panevėžys.

“At the beginning of 2025, the country’s housing market is showing impressive results. After a very strong growth in housing transactions in January and February this year, the increase in the number of transactions continued in March. According to the data of the State Enterprise Centre of Registers, in March this year, 19% more houses were purchased in the country and 20% more apartments were purchased than in the same month in 2024. And for example, in the capital of the country, January, February and March were historically the most productive months in the segment of older apartments, compared to the same months of the previous year.

The fact that the housing market is recovering rapidly is also reflected in the volume of new mortgage originations. According to the data of the Bank of Lithuania, in February 2025, the volume of new housing loans issued in Lithuania reached record highs – almost EUR 240 million, or 92% more than a year ago. The very good indicators of the housing market have also given optimism to home sellers, who are trying to sell their homes at ever higher prices.

But just when homebuyers seemed to have adjusted to the geopolitical tensions and could now plan more confidently in a falling interest rate environment, the world was shaken by the news that the US was imposing tariffs on imports to this country. Global trade markets are suddenly facing extreme challenges that could unbalance trade relations between countries and negatively affect the development of both the European Union and the Lithuanian economy. Especially in the event of a further escalation of US-China trade. Although it is difficult to assess the real impact of the duties imposed and their continuation at this stage, it is clear that this is a negative message for consumers and especially for those who are planning to make larger commitments, for example, in the case of home purchases.

According to the State Data Agency, the country’s consumer confidence indicator fell by 4 percentage points between February and March 2025, indicating that people’s expectations of their financial situation or the general economic situation of the country have deteriorated slightly. This may also be related to the recent, particularly active discussions on the planned changes to the Lithuanian tax system, which would inevitably increase the tax burden on both businesses and individuals. Meanwhile, the deteriorating expectations of the population may have an impact on the housing market, which is currently looking very strong, in terms of slowing down the pace of market recovery or the growth of sales prices”, said Raimondas Reginis, head of market research for the Baltics at Ober-Haus.

Full review (PDF): Lithuanian Apartment Price Index, March 2025

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.4% in February 2025. The annual apartment price growth in the biggest cities of Lithuania was 4.1% (a 4.0% increase was recorded in January 2025).

In February 2025 apartment prices in Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys increased by 0.3%, 0.1%, 0.8%, 0.8% and 0.9%, respectively, with the average price per square meter reaching EUR 2,670 (+7 EUR/sqm), EUR 1,822 (+2 EUR/sqm), EUR 1,754 (+13 EUR/sqm), EUR 1,168 (+10 EUR/sqm) and EUR 1,147 (+10 EUR/sqm).

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 3.2% in Vilnius, 4.1% in Kaunas, 6.2% in Klaipėda, 6.6% in Šiauliai and 6.7% in Panevėžys.

‘As predicted, a rapid annual growth in the number of housing transactions is recorded at the beginning of 2025. According to the data of the State Enterprise Centre of Registers, 40% more apartments were purchased in the country in January this year and 39% more in February this year than in the same month in 2024. It should be noted that in the first half of 2024 the housing market activity was still in a downward phase and the number of housing purchases had fallen to the lows of the last decade, so the low comparative base allows for a high relative growth this year.

However, the rapid increase in the number of transactions is not only due to the extremely low figures for the first half of 2024, but also to the apparent recovery of the market. The fall in lending rates, rising personal incomes and the recent positive developments in the housing market have brought back at least some of the previously hesitant buyers back to the market. For example, February this year was historically the most productive month in the older apartment segment (compared to February of the previous years). The performance of the primary apartment market in the country’s major cities also shows that the housing market has entered a period of sustained recovery.

Sales prices continue to climb at a moderate pace, with smaller cities in the country experiencing slightly higher price growth. For example, the record high price level in the capital city (especially when taking into account the purchasing power of the population) is somewhat limiting the faster price growth, while smaller cities have a noticeably lower price level and a higher potential for relative price growth.

In the short term, we should also see a fairly rapid statistical recovery of the market (especially compared to the previous year), but in the second half of 2025 activity growth should not be as strong. The recovery of the housing market, which started in mid-2024, has already created a higher level of activity. Meanwhile, house prices should continue to grow at a similar pace as in the last few years. Despite the market-enhancing fundamentals, overall buyer sentiment is likely to continue to be dampened by geopolitical tensions‘, said Raimondas Reginis, head of market research for the Baltics at Ober-Haus.

Full review (PDF): Lithuanian Apartment Price Index, February 2025

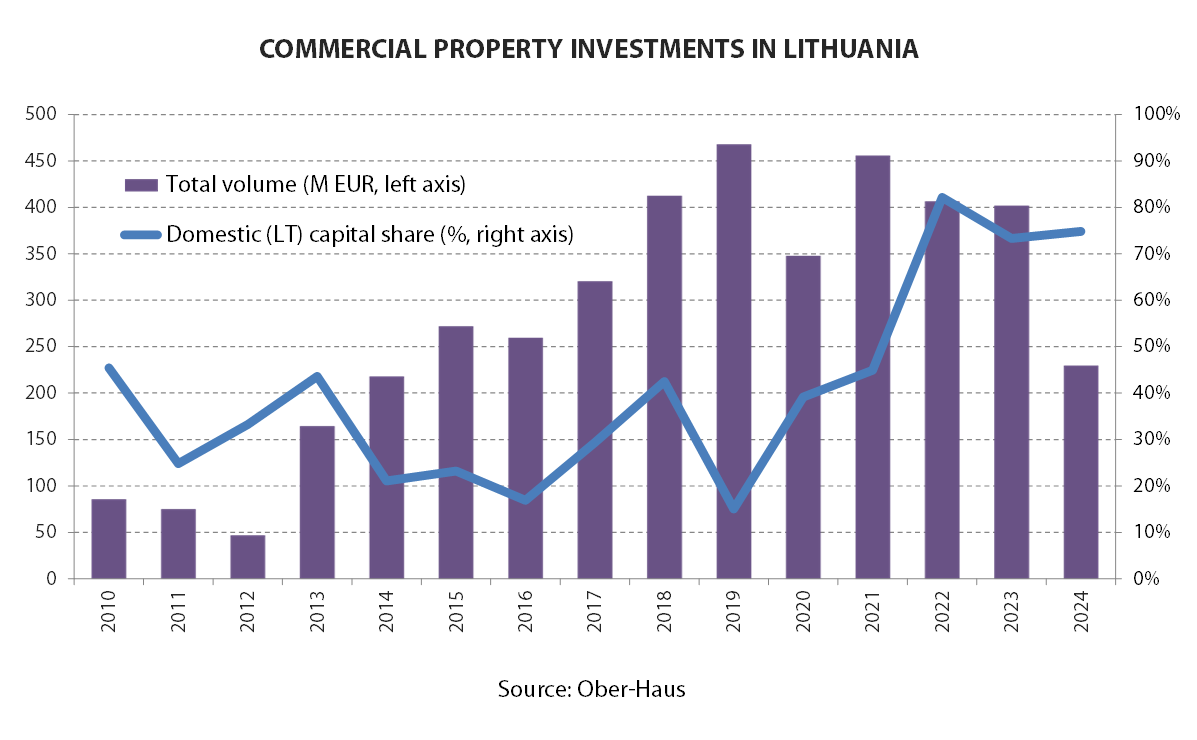

The general sentiment in the Lithuanian commercial property market in 2024 is well reflected in the volume of investments, which has declined to the levels last seen in 2014. According to the data of Ober-Haus, in 2024, the value of modern cash-flow commercial property (modern office, retail and industrial objects with the value of at least EUR 1.5 million) acquired amounted to EUR 230 million. This means that the annual volume of investments declined by 43% compared to 2023 or 2022.

‘In 2024, only small and medium-sized transactions were recorded in Lithuania, whereas there had been no acquisitions of larger transactions at all. For the first time after a lengthy period, the value of the largest deal did not exceed EUR 30 million‘, said Raimondas Reginis, head of market research for the Baltics at Ober-Haus. According to Ober-Haus, deals up to EUR 10 million in value represented 40% of total investments in Lithuania, whereas deals valued at EUR 10–30 million – the rest (60%).

Retail properties attracted the largest share of investments, with investors primarily focusing on supermarkets

The largest portion of investments befell to retail properties with EUR 134 million or 58% of all investments in commercial property in Lithuania spent for acquisitions. In 2024, this segment was noted for the most significant acquisitions as well as the biggest number of deals.

For example, a fund managed by Estonian company Eften Capital purchased Una retail park, opened in the middle of 2023, at the northern part of Vilnius (nearby Molėtų Road). In the meantime, a fund of Latvian investment management company, Provendi Asset Management, bought in Panevėžys the DYI shopping centre of the construction materials and household products chain Depo. Besides these larger transactions, in the retail segment, buyers were especially actively seeking small-format supermarkets (1,500–2,500 sqm), operated by the major grocery store chains. During 2024, as many as 10 objects of such format were purchased, while the largest transaction involved the sales of four newly constructed Lidl stores to a fund managed by the investment management company, DIFF Assets.

‘Broad geographical distribution also suggests that this kind of property remains particularly attractive to investors. Stores were purchased in the largest cities as well as in smaller towns of the country: Panevėžys, Molėtai, Alytus, Marijampolė, Prienai, Jurbarkas, and Vilnius and Klaipėda districts. This indicates that investors trust in the continued success of their tenants’ operations in such properties and are paying record-high prices for them, even during a period of weak market activity’, Mr Reginis said.

In 2024, office segment attracted EUR 70 million in investment

The second largest share of investments in 2024 went to the segment of office premises, with EUR 70 million spent or 31% of total investment in commercial property made in Lithuania.

The largest transaction in the office segment was concluded in the second half of the year, when the sale of a complex of administrative buildings on A. Juozapavičiaus Street and Žvejų Street in Vilnius was announced. Buildings with 16,000 sqm of floor space and a land plot in the central part of the city were bought by the real estate developer Realco, which sees new development opportunities in this area. In the middle of 2024, a fund of investment management company ZeroSum Asset Management purchased a complex of three office buildings from the Norwegian capital company AMG Property in Švitrigailos Street, in Vilnius. In the meantime, at the beginning of the year, a real estate development company Eriadas together with the closed-end investment fund for informed investors DIFF Develop acquired the buildings of the insurance company Ergo in Geležinio Vilko Street, in Vilnius.

‘The number of investment deals made and prices of property acquired in the recent years suggest that investors are still wary of the office segment. The slowing expansion of the business and growing level of vacant office premises reduced the attractiveness of this segment and led the investors to approach the assessments of this real estate segment more conservatively’, Mr Reginis explained. This is particularly the case in the capital city of the country, where office development has not stopped and the vacancy rate of premises over the last two years hopped from 5.9% to 8.8%, while the total area of vacant premises for the first time in history exceeded 100,000 sqm.

The remaining (11%) smallest share of investments traditionally went to the acquisition of warehousing and manufacturing premises. The largest deal of 2024 was concluded in Kaunas, where the fund of the investment company Eika Asset Management sold a 5,600 sqm logistics building to its tenant, Camelia pharmacy chain. Other smaller acquisitions were carried out in Vilnius and Kaunas and Klaipėda regions.

Local capital continues dominating the investment market

The most recent annual data suggest that local capital retains its predominant position in the commercial real estate transactions’ market. Sharp growth of local capital investments share recorded in the Lithuanian investment transactions’ market since 2022 remained at record high in 2024, too. According to Ober-Haus data, in 2022, the share of capital held by Lithuanians in investment transactions shot to 82%, in 2023 accounted for 73%, and in 2024 – for 75%. ‘For instance, over the period of 2012–2021, the share of local investors comprised 37% in total investments. This suggests that foreign investors have not yet returned to our country’s real estate market, and currently, only investors from other Baltic States – Latvia and Estonia – are interested in investing’, the analyst said.

More positive changes can finally be expected after a deep fall

Recent prices of commercial real estate suggest that there is still a wide variation in prices, both across individual segments and in terms of the quality of the properties. According to Mr Reginis, buyers are especially cautious about the prospects – potential lease revenues and likely additional investments – of older objects and those located in smaller towns of the country. Consequently, they seek to acquire such objects with the maximum yield possible that might even reach double figures (e.g. 10–11%). ‘In the meantime, new objects in the capital or strategically attractive locations of other cities receive greater interest from the buyers. Fully occupied objects guarantee for the buyers an indexed cash flow and minimum investments to the object maintenance in the medium or lengthier period; hence, such objects even now can be acquired with a 6.5–7.0% yield. Smaller objects, such as stand-alone supermarkets, can be bought with a yield slightly below 6.0%’, the representative of Ober-Haus explained.

In view of the overall situation in the commercial real estate market and specifically in the investment transactions’ market in 2024, more positive developments can be expended in 2025.

‘Irrespective of the persisting geopolitical tensions, the growing economy of the country and decreasing interest rates might enliven the business (tenants) expansion and boost up the overall activity of the commercial real estate market – in particular, in the segment of office or warehousing premises. For instance, as of the middle of 2024, clear positive trends have been seen in the housing market. This would enhance the investor confidence in the commercial real estate market, and higher activity could be expected in the investment transactions’ market as well. We are unlikely to see a more active return of foreign investors to our market; however, local investors should act with more courage’, Mr Reginis said.

In 2024, the market for new-build apartments in major cities reached a turning point, when sales growth started to pick up again after a two-year slump in the primary and secondary apartment market. According to Ober-Haus data, compared to 2023, in 2024 there will be 43% more apartments sold in the primary market in Vilnius, 40% more in Kaunas and 44% more in Klaipėda. The year-on-year decline in mortgage interest rates, stabilisation of sales prices and various sales promotion strategies of developers have brought back at least some of the delayed buyers to the new-build housing market.

“On the one hand, we are seeing an increase in housing market activity, while on the other hand, the volume of apartments being developed for sale in some major cities has fallen to historic lows,” says Raimondas Reginis, head of market research for the Baltics at Ober-Haus. The biggest drop in development was recorded in the country’s capital, where even fewer apartments were built during the year than forecast a year ago. According to Ober-Haus, in 2024 developers in Vilnius will build 2,589 apartments for sale, or 47% less than in 2023. “And this is the lowest rate in the last 10 years. The drastic drop in buyer activity on the primary market between 2022 and 2023 has forced most developers to halt their investments or slow down the pace of development. As the construction of apartment buildings usually takes about 1-2 years, we are therefore recording a historically very modest number of completions in 2024.

At the same time, the rental market in 2024 has seen a fairly solid addition of new housing from investors developing exclusively rental housing projects. During the year, four new rental projects (Liv_in Vilnius New Town, Eften Living Vilnius, B10, Hedonistas) were opened in the capital, bringing the total number of rental units on the market to more than 380, bringing the total number of rental and professionally managed units in Vilnius to almost 2,500.

“The highest volumes of such housing development in the capital of the country were recorded in 2022-2023. Despite the slowdown in the real estate market as a whole over the last few years, the rental segment in the country’s major cities remains very active. The growing population in the country’s major cities and the still low level of housing affordability encourage both large and small investors to invest in the rental segment,” says R. Reginis.

In 2024, two thirds of apartments will be built in four districts of Vilnius

The developers have built new flats in 12 wards of Vilnius city over 2024. The four wards with the most developers’ attention were the four wards where two thirds of all apartments were built: Žirmūnai sen. (25.6%), Pilaitė sen. (18.6%), Naujamiestis sen. (14.0%) and Pašilaičiai sen. (8.8%).

“In recent years, quite active development of multi-flats has been taking place in the northern part of Žirmūnai, on the site of the former Kuro Apparatus factory, and in the surrounding areas. The attractive location of this area in the city and its high development potential have encouraged investments in this area of the city, which will obviously continue to expand in the future. The relocation of the current Verkiai bus park and the planned upgrading of 9 hectares of the site for public use should be a particular boost,” says Mr Reginis.

As in 2023, in 2024 the Senamiesčio district was characterised by a very modest volume of completed multi-family projects (2.0% of the total number of flats constructed in the year).In 2024, the construction of the last stages of the Paupis district was actually completed, which completed the development of one of the largest conversion projects in the capital in the Paupis district. A total of around 900 apartments and various commercial facilities have been built in this quarter, with an investment of EUR 200 million. Reginis points out that the Old Town has limited opportunities for new development and that more expensive projects take much longer to complete than typical projects in other parts of the city. “However, more than ten projects of various sizes are planned to be completed in this district between 2025 and 2026, which will significantly add more expensive housing to the market”, he says.

The average size of apartments in the capital remained below 50 sqm

In 2023, for the first time, the average floor area of flats built for sale in multi-apartment buildings did not exceed 50 sqm (49.9 sqm). According to Ober-Haus data, in 2024, the average area of an apartment in multifamily flats built in Vilnius decreased even further and amounted to 49.5 sq m. According to Reginis, the record low average area could be caused by the very limited number of higher class projects completed in 2024. “Such projects usually design much more spacious apartments for buyers, and the average area of apartments in an apartment block can reach even 80-100 sqm. However, in 2024, the majority of the apartment blocks built were in the economy and middle class, which, however, were dominated by smaller apartments. For example, in the capital city, at least four apartment blocks were built with an average apartment area of less than 40 sqm,” the analyst says.

Taking into account that in 2025-2026 more high-end projects will be implemented in the capital, and it is already irrational to design even more flats with smaller floor area in apartment blocks (due to the higher density of the population, the level of comfort of living will deteriorate, and the overall attractiveness of the project will be reduced at the same time), it is highly probable that the average floor area will not decline any further, and will return to the level of the period of 2018-2022 (50-53 sq.m.) at least.

Half of the apartments in the capital are built in A++ energy class apartment buildings

The data collected by Ober-Haus show that out of the apartments built for sale in the capital of the country in 2024, apartments in A++ energy class apartment buildings will account for 49.9% (24.1% in 2023). “Although the requirement to comply with the requirements of the A++ energy efficiency class has come into force for newly constructed buildings as of 1 January 2021 (when the building permit is applied for), we can see that no more than half of such apartment blocks will be built in Vilnius in 2024,” points out Reginis.

In 2024, 22.4% of apartments in A+ energy class apartment buildings (55.3% in 2023), and 21.2% of apartments in A-class buildings (12.2% in 2023). The remaining share of apartments (6.5%) was in B or lower energy class apartment blocks (8.4% in 2023). “There are still some new or reconstructed apartment blocks for sale on the market, which are also issued with B energy performance certificates. These are mostly projects developed under previously issued building permits, as developers do not want to waste time on the coordination of new project solutions and permitting procedures,” explains the Ober-Haus representative.

Predictions have been confirmed – 45% less built in Kaunas

The forecasts made a year ago about the decline in the volume of apartment building in Kaunas in 2024 have been fully confirmed. According to Ober-Haus data, in 2024 developers in Kaunas will build 834 apartments for sale, or 45% less than in 2023, which was a year of record-breaking construction volumes.

“Just like in the capital city, developers in Kaunas have reacted to the reduced demand for housing and significantly reduced the pace of development. This is especially visible when compared to the record year of 2023, when as many as 1,500 apartments were built for sale in Kaunas. And historically speaking, in 2024, the volume of construction of apartments for sale returned to the level of 2019-2020,” says Reginis. In total, in 2024, buyers could build in 27 different projects (counting the continuous phases of projects).

In 2024, developers built apartment blocks in various locations in and around the city, but the Šančiai sub-district stood out the most, with 22% of the total number of apartments built. For example, two new apartment blocks (over 80 flats) were built on the area of the former military barracks near A. Juozapavičiaus Ave., completing the conversion of this area. Over the years, new buildings and old buildings have been built and reconstructed in this area, housing the city’s residents and various businesses. There has also been quite a lot of construction activity in other districts of the city, such as Dainava, Vilijampolė, Šilainiai and Žaliakalnis.

Klaipėda’s development rates increase in 2024

According to Ober-Haus data, in 2024 developers in Klaipėda will build 478 apartments for sale or 19% more than in 2023. Unlike Vilnius and Kaunas, Klaipėda is experiencing an increase in construction volumes, but the city’s multifamily development remains relatively modest but stable. However, in 2024, the number of apartments built in the port city was the highest since 2009.

Klaipėda is typically home to smaller and medium-sized developments, giving buyers a choice of different projects. For example, in 2024, buyers in Klaipėda could build in 13 different projects (including continuous phases).

“It is encouraging that buyers have a wider choice of housing in the central part of the city or in the Old Town area. In addition to smaller projects in this part of the city, larger and higher class projects are finally being implemented,” says R. Reginis. In 2024, the construction of the first two blocks of flats (about 90 apartments) in the Bastionų namai project near the Danube River was completed, and the construction of the other phases is continuing. Also in 2025, construction of the first phase of Memel City should be completed, with around 100 apartments and a business centre to be built at the junction of the River Danube and the Curonian Lagoon.

Recent demographic trends in Klaipėda are also quite positive. According to the State Data Agency, the number of permanent residents in Klaipėda City Municipality has been growing for the fourth year in a row, and over the last five years the population of the port city has increased by 5.7%, or slightly more than 8,700 residents. Meanwhile, the growth rate of Klaipėda District remains noticeably faster – the population grew by 26.0% or almost 14,300 inhabitants over the same period.

Development trends in major cities in 2025 are different

Despite the recovery of the housing market that started to be recorded in the second half of 2024, developers in the country’s major cities have not yet started construction of new projects on a larger scale during the year. For smaller developers, the biggest challenge was and still is the very limited availability of financing, while larger developers have started to implement those projects for which building permits have been obtained.

A survey of the country’s major developers prepared by the LNTPA at the beginning of 2025 (the Real Estate Market Expectations Index) showed that the prospects for the housing sector are currently viewed as very good. In 2025, developers are willing to increase the volume of development, but bureaucratic disturbances, unfavourable legal framework, and smooth implementation of new regulations are identified as the biggest obstacles to development.

According to Reginis, despite the change in market sentiment for the better, the volume of completed apartments in 2025 will not be abundant, and the trends in major cities are different. Taking into account the currently under construction apartment blocks and their construction progress, Ober-Haus estimates that in 2025, a total of about 3,300 apartments will be built for sale in Vilnius, or 27% more than in 2024. Meanwhile, in Kaunas, a further decline in construction volumes is forecast, where around 680 apartments are expected to be built in 2025 (18% less than in 2024). In Klaipėda, meanwhile, construction volumes are expected to maintain their normal pace in 2025, with around 400 apartments to be built for sale (16% less than in 2024).

After a very unbalanced housing market period from 2021 to 2023, in 2024 the country’s major cities have finally maintained a healthy balance between the number of apartments built and the number of apartments sold. According to Ober-Haus estimates, in Vilnius, Kaunas and Klaipėda the total number of apartments built was 3,900, while the number of apartments sold on the primary market was around 4,400.

“The relatively fast growth of sales volumes on the primary market shows that buyers are returning to the market of new-build apartments and are much more confident in their decision to buy a home. At the same time, the actual construction volumes are still at a low level and if the demand for housing remains as active this year as it was at the end of 2024 or the beginning of 2025, a shortage of housing may be felt in the second half of 2025,” R. Reginis believes.

The Kaunas market may face greater challenges, as the rate of development of apartments here has been declining for two years in a row (taking into account the 2025 forecasts). The Vilnius market, which has the highest market recovery potential (in nominal terms), and the actual construction volumes in 2025 will remain at a relatively low level (3,300 apartments). Based on the current sales rate, it is likely that around 4,400 new apartments will be sold on the Vilnius primary market in 2025, which means that statistically there will be a shortage of around 1,100 apartments. “Looking at the rebalanced market in 2021-2023, such a shortage is not yet critical, but it does signal an unfavourable trend for the market. And especially for home buyers. It is therefore important that developers are prepared to respond to a faster market recovery. This means starting to build more projects in 2025, so that at least there is no housing shortage in 2026 or 2027,” says R. Reginis.

A. Juozapavičiaus Street, Kaunas, the last apartment in the project “Beržų namai” was sold, the concept of which was developed and successfully realised by Ober-Haus. All the apartments have already been occupied, and the completion of the project has become a significant event in the rapidly modernising Žemieji Šančiai district.

Two apartment buildings have been designed on a plot of almost 0.43 hectares, with 72 two- to three-room apartments of 45-63 square metres. The project includes 41 underground and 32 above-ground parking spaces, bicycle storage and storage rooms, and a private courtyard.

“From the very beginning of the sale, we have felt great interest from buyers – the reason for this is both its exceptional location and the lack of quality housing in Kaunas,” says Svajūnas Šarauskas, Manager of the Kaunas office of Ober-Haus.

The houses were built in the growing and rapidly changing Žemieji Šančiai district, in a quiet and green part of A. Juozapavičiaus Avenue. “Beržų namai has contributed to the development of the area by landscaping the environment, greening and fencing the yard, and installing a children’s playground. “Beržų namai has not only added to the landscape of the modernising district, but has also encouraged the development of other housing projects in this part of the city.

“The location of the project dictated the architectural and qualitative requirements. Particular attention was paid to the naturalness and quality of building materials. Therefore, although the project envisaged A+ class apartment blocks, the certification has resulted in the buildings being given an even higher energy class of A++,” says S. Šarauskas.

Ober-Haus advised on pricing and concept development, developed and implemented the marketing strategy and managed the sales process. The investor of the project is UAB J29C and the main construction works were carried out by UAB Agda.

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.5% in December 2024. The annual apartment price growth in the biggest cities of Lithuania was 3.6%. The average annual apartment price growth in 2024 (January – December 2024 compared to January – December 2023) reached 2.9%.

In December 2024 apartment prices in Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys increased by 0.6%, 0.7%, 0.1%, 0.5%, and 0.4%, respectively, with the average price per square meter reaching EUR 2,646 (+14 EUR/sqm), EUR 1,819 (+12 EUR/sqm), EUR 1,719 (+2 EUR/sqm), EUR 1,147 (+7 EUR/sqm), and EUR 1,123 (+4 EUR/sqm).

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 2.8% in Vilnius, 4.8% in Kaunas, 4.8% in Klaipėda, 4.4% in Šiauliai and 3.9% in Panevėžys.

“In 2024, the country’s housing market was characterised by a volatile mood. A decline in market activity was recorded until the middle of the year, before recovering in the second half of the year. However, the total number of registered transactions in the country in 2024 remained almost the same as in 2023. Meanwhile, sales prices of apartments have been slowly moving upwards, increasing by 3.6% over the year in the country’s major cities, i.e. slightly faster than in 2023 (1.7%).

However, the average annual price change in 2024 was one of the lowest in the last decade, at 2.9%. In 2024, the average annual change slowed down considerably compared to the previous year, as in 2023, the sales prices of apartments have largely stopped rising and a high comparative base has been formed. In 2024, the trajectory of sales prices of apartments again broadly followed the general inflation trend, although house prices still rose slightly faster than the prices of other consumer goods and services in the country.

In 2024, the biggest changes were recorded in the primary market of metropolitan apartments. Compared to 2023, Vilnius, Kaunas and Klaipėda saw a 40% increase in the number of flats sold on the primary market. In 2024, the rapid growth of new-build apartment sales volumes in the primary market was driven by the extremely low activity rates in 2023 and returning buyers to this market. Also in 2024, new-build apartments appreciated at twice the rate of older construction. On average, new-build flats in the country’s major cities increased in price by 5.4%, while older flats increased in price by 2.3%.

In the second half of 2024, the general mood on the housing market improved, as positive news dominated the public space: a consistent decline in interest rates on loans, a recovering housing sales market, rising real personal income levels due to falling inflation and positive prospects for the overall development of the country’s economy. This has encouraged potential homebuyers to become more active in their purchasing decisions, and it seems that the positive trends in the housing market will continue in 2025.

This year is likely to see a rapid increase in housing market activity. With the number of housing purchases in the first half of 2024 having fallen to the lows of the last decade, the low comparative base provides the conditions for strong relative growth. At the same time, house prices, which have reached record highs, remain the biggest challenge for potential homebuyers even in a falling interest rate environment. Therefore, the pace of house price growth in 2025 will also depend to a large extent on the growth of real incomes of the population, especially of the middle class – who are the most important players in the housing market and largely shape the overall level of house prices in the country,” says Raimondas Reginis, Ober-Haus Research Manager for the Baltics.

Full review (PDF): Lithuanian Apartment Price Index, December 2024

“As the level of house prices has been rising slowly and at a similar pace in all the country’s major cities, we can see that, in the longer term, the price differential between the major cities has remained broadly stable. The difference in prices between the national capital and the rest of the major cities can be up to two times higher for a typical house. For example, in November 2024, buyers in the most popular districts of Vilnius paid an average of EUR 103,000 for an old two-room apartment. The property bought for this amount is a tidy or better furnished apartment of 49 sqm in a block of flats built in 1977.

Meanwhile, buyers in Kaunas bought the same dwelling in November this year for an average of EUR 76,000, and in Klaipėda – EUR 70,000. At the same time, in Šiauliai and Panevėžys the price level of the same dwelling is 25-30% lower than in Kaunas and Klaipėda, and almost twice as low as in the capital of the country, i.e. EUR 54,000 and EUR 51,000 respectively.

Old-built housing remains very popular as it is the most affordable for those looking for a home in the city. Although the statistical wages in smaller cities are noticeably lower than, say, in the capital, the opportunities to buy the most popular type of housing are still better. And this is a significant advantage of smaller cities over the country’s largest cities,” says Raimondas Reginis, Ober-Haus Research Manager for the Baltics.

Full review (PDF): Lithuanian Apartment Price Index, November 2024

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.3% in October 2024. The annual apartment price growth in the biggest cities of Lithuania was 3.4% (a 3.0% increase was recorded in September 2024).

In October 2024 apartment prices in Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys increased by 0.2%, 0.5%, 0.3%, 0.4% and 0.2% respectively, with the average price per square reaching EUR 2,622 (+5 EUR/sqm), EUR 1,805 (+10 EUR/sqm), EUR 1,713 (+5 EUR/sqm), EUR 1,142 (+5 EUR/sqm) and EUR 1,120 (+2 EUR/sqm).

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 2.2% in Vilnius, 4.8% in Kaunas, 5.8% in Klaipėda, 3.5% in Šiauliai and 4.3% in Panevėžys.

“Over the last two years, the trend in sales prices has remained broadly unchanged, with overall price levels continuing to rise slowly. We can see that the decline in housing market activity, which has continued for more than two years, has not lowered price levels, but has led to a marked increase in the period of home sales and a slowdown in the rate of price growth. Most sellers have adapted to the changed market situation by waiting patiently for buyers or by stopping the sales process altogether, and only a small number of sellers, especially those willing to sell faster, have had to give significant discounts to homebuyers.

However, the figures for the second half of this year have already given hope to home sellers that the period of the lowest market activity is behind them. October is the fourth month in a row when the number of flats and houses sold in the country has increased compared to the same period a year ago, indicating that buyers have started to make more active decisions on home purchases. According to the data of the State Enterprise Centre of Registers, in October this year the number of purchases of housing (apartments and houses) in the country was 19.4% more than in September this year and 20.2% more than in the same month a year ago. At the same time, October was the most active month on the housing market since the end of 2021.

However, despite the housing market recovery that is beginning to be recorded after a long pause, there is still no greater optimism in the housing market and buyers remain cautious and reluctant to make quick decisions or to overpay for a home. The steady decline of EURIBOR from the end of 2023 has given optimism to market participants, but homebuyers should have first seen a real reduction in the servicing burden on future or existing mortgages. If we look at newly issued mortgages, according to the Bank of Lithuania, the average interest rate on newly concluded mortgages has fallen by almost one percentage point over the year – from 5.79% to 4.85%. Meanwhile, interest rates on existing mortgages, and thus loan repayments, are not falling as fast as most people prefer to recalculate interbank interest rates (EURIBOR) every 6 months. The pace of recovery of the housing market will probably depend on how quickly the majority of potential buyers actually feel that mortgage loans are easier to service.

In the meantime, house price dynamics remain favourable for homebuyers. In 2024, the average annual change in the sale price of apartments in the country’s major cities will be one of the lowest in the last eight years,” says Raimondas Reginis, Ober-Haus Research Manager for the Baltics.

Full review (PDF): Lithuanian Apartment Price Index, October 2024

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.1% in September 2024. The annual apartment price growth in the biggest cities of Lithuania was 3.0% (a 3.0% increase was recorded in August 2024).

In September 2024 apartment prices in Kaunas, Klaipėda and Panevėžys increased by 0.3%, 0.4% and 0.7% respectively, with the average price per square reaching EUR 1,795 (+6 EUR/sqm), EUR 1,708 (+6 EUR/sqm) and EUR 1,118 (+9 EUR/sqm). In the same month, apartment prices in Vilnius decreased by 0.1% and the average price per square meter dropped to EUR 2,617 (-3 EUR/sqm). Apartment prices in Šiauliai did not change during the month and the average price per square meter remained at EUR 1,137.

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 1.9% in Vilnius, 4.1% in Kaunas, 5.9% in Klaipėda, 3.1% in Šiauliai and 3.7% in Panevėžys.

Full review (PDF): Lithuanian Apartment Price Index, September 2024

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.1% in August 2024. The annual apartment price growth in the biggest cities of Lithuania was 3.0% (a 3.2% increase was recorded in July 2024).

The Ober-Haus Lithuanian apartment price index (OHBI), which follows changes in apartment sale prices in the five biggest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys) increased by 0.1% in August 2024. The annual apartment price growth in the biggest cities of Lithuania was 3.0% (a 3.2% increase was recorded in July 2024).

In August 2024 apartment prices Vilnius, and Šiauliai increased by 0.2% and 0.6% respectively, with the average price per square reaching EUR 2,620 (+6 EUR/sqm) and EUR 1,137(+6 EUR/sqm). In the same month, apartment prices in Kaunas and Klaipėda decreased by 0.1% and the average price per square meter dropped to EUR 1,789 (-1 EUR/sqm) and EUR 1,702 (-2 EUR/sqm) respectively. Apartment prices in Panevėžys did not change during the month and the average price per square meter remained at EUR 1,109.

In the past 12 months, the prices of apartments increased in all the biggest cities in the country: 1.9% in Vilnius, 3.7% in Kaunas, 5.7% in Klaipėda, 3.4% in Šiauliai and 3.3% in Panevėžys.

“The Lithuanian housing market is already trying to recover from the stagnation that has gripped it, which lasted basically until mid-2024. August is the second month in a row when the number of apartments and houses sold in the country is higher than in the same period a year ago. According to the data of the State Enterprise Centre of Registers, in July this year, the number of purchases of dwellings (flats and houses) was 10.7% higher, and in August it was 6.3% higher than in the same month a year ago. These data show that the housing market has already reached its lowest point of activity and homebuyers are slowly returning to the market.

However, the positive changes in housing activity recorded are hardly visible in practice on the market, as the overall volume of home purchases remains at a relatively low point and the negotiating positions of home sellers have not improved substantially. This is confirmed by the prices of old and new-build flats in the last few months, which have remained stable in the major cities. Buyers currently still lack confidence both in their financial capacity and in the prospects of the housing market and are taking their purchasing decisions slowly. It is likely that buyers will return to the market slowly and this will require not only a further steady decline in interest rates, but also more positive news in the country’s economy and real estate market,” says Raimondas Reginis, Ober-Haus Research Manager for the Baltics.

Full review (PDF): Lithuanian Apartment Price Index, August 2024